Earnings & Stock Announcements

Origin Bancorp, Inc. Reports Earnings For Fourth Quarter and 2020 Full Year

RUSTON, Louisiana (January 27, 2021) - Origin Bancorp, Inc. (Nasdaq: OBNK) ("Origin" or the "Company"), the holding company for Origin Bank (the "Bank"), today announced net income of $17.6 million for the quarter ended December 31, 2020. This represents an increase of $4.5 million from the quarter ended September 30, 2020, and an increase of $4.7 million from the quarter ended December 31, 2019. Diluted earnings per share for the quarter ended December 31, 2020, were $0.75, up $0.19 from the linked quarter and up $0.20 from the quarter ended December 31, 2019. Pre-tax pre-provision earnings for the quarter were $28.3 million, a decrease of 5.4% on a linked quarter basis, and a 54.1% increase on a prior year quarter basis, while the efficiency ratio improved to 57.9%, an 867 basis point decrease from the quarter ended December 31, 2019.

Net income for the year ended December 31, 2020, was $36.4 million, representing a decrease of $17.5 million compared to the year ended December 31, 2019, primarily reflecting a year-over-year increase in provision expense, offset by higher net interest income and noninterest income. Diluted earnings per share for the year ended December 31, 2020, was $1.55, representing a decrease of $0.73 from diluted earnings per share of $2.28 for the year ended December 31, 2019.

“I am extremely proud that our employees continue to remain committed to our culture and creating opportunities out of challenges to better serve our customers and communities", said Drake Mills, Chairman, President, and CEO of Origin Bancorp, Inc. “We believe our company has shown amazing resiliency, and we are strategically positioned to build sustainable, long term value for our stakeholders and continue to help the economic recovery across our footprint.”

Financial Highlights

- Net income was $17.6 million for the quarter ended December 31, 2020, achieving a historic high compared to $13.1 million for the linked quarter and $12.8 million for the quarter end December 31, 2019.

- Net interest income also achieved a historic high, reflecting $51.8 million for the quarter ended December 31, 2020, compared to $50.6 million for the linked quarter and $44.1 million for the quarter ended December 31, 2019.

- Diluted earnings per share for the quarter ended December 31, 2020 were $0.75, compared to $0.56 for the linked quarter and $0.55 for the quarter ended December 31, 2019.

- Provision expense was $6.3 million for the quarter ended December 31, 2020, compared to provision expense of $13.6 million for the linked quarter and $2.4 million for the quarter ended December 31, 2019.

- Total LHFI were $5.72 billion at December 31, 2020, an increase of $112.1 million, or 2.0%, from September 30, 2020, and an increase of $1.58 billion, or 38.2%, from December 31, 2019.

- Total deposits at December 31, 2020, were $5.75 billion, a decrease of $184.6 million, or 3.1%, from September 30, 2020, and an increase of $1.52 billion, or 36.0%, from December 31, 2019.

- The Company completed an offering of $80 million in aggregate principal amount of subordinated notes due 2030 in October 2020. The notes qualify as Tier 2 capital for the Company and approximately $51.0 million was contributed to the Bank and qualifies as Tier 1 capital for regulatory capital purposes for Origin Bank.

Coronavirus (COVID-19)

Origin has continued to meet customers' needs while keeping the safety and well-being of the Company's employees and customers as its top priority. The Company implemented a COVID-19 hotline and a temporary pandemic Paid Time Off policy to assist employees. The Company's offices and all branches remained open with all drive-thrus fully operational. The Company has maintained social distancing measures for its employees working in the Company's offices, including appointment-only restricted lobby access and requiring employees to wear face masks unless working in an office or other location that permits social distancing. The Company has also enhanced its sanitation protocols, implemented return-to-work screening protocols following potential exposures, as well as other measures consistent with applicable federal, state, and local guidelines to promote the safety and health of its employees and customers. To allow for more normalized customer operations, the Company has installed thermal kiosks for temperature checks at the entrance of each location and will evaluate any additional safety protocols to allow unrestricted lobby access in the future, if the circumstances allow.

Credit Quality

The COVID-19 pandemic has continued to have a severe impact on the U.S. economy leading to elevated unemployment levels and a recession. The Company's results for 2020 have been impacted by higher provision expense resulting in an increase in the allowance for credit losses due to the COVID-19 pandemic and the uncertainty surrounding the economic outlook.

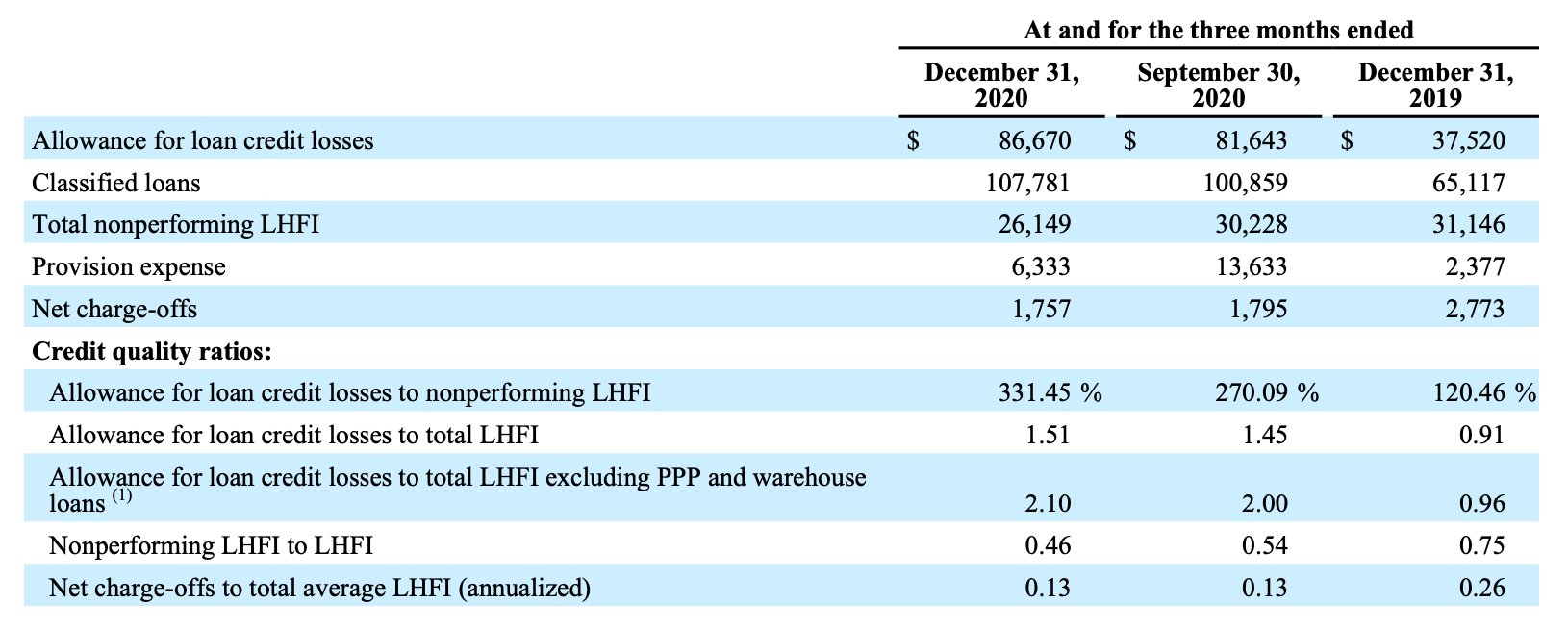

The table below includes key credit quality information:

The decrease in provision expense compared to the linked quarter reflects an improvement in forecasted economic conditions. While we are seeing some improvements in economic forecasts, there remains a heightened level of uncertainty, particularly related to the first half of 2021, regarding the economic impact of increasing COVID-19 cases and the deployment of a vaccine. The increase from December 31, 2019, was primarily due to the decline in overall economic conditions as a result of the aforementioned uncertainty resulting from the pandemic and the change in accounting methods from incurred loss to expected loss under the implementation of Accounting Standards Update ("ASU") No. 2016-13, Financial Instruments - Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments ("CECL").

The Company continues to closely monitor those industry sectors that could experience a more protracted recovery from the current economic downturn, specifically the sectors of hotels, energy, non-essential retail, restaurants, and assisted living. Excluding PPP loans, at December 31, 2020, the Company had $538.6 million, or 10.4%, of its LHFI invested in these sectors and, while the Company has increased its allowance for loan credit losses related to these sectors, the allowance is a current estimate and may be subject to change. Nonperforming LHFI in these sectors were $5.9 million at December 31, 2020, while past due LHFI, defined as loans 30 days or more past due, as a percentage of LHFI in these sectors, excluding PPP loans, was 1.0% at December 31, 2020. Loans in COVID-19 related forbearance totaled $97.7 million and represented 1.9% of LHFI, excluding PPP loans, at December 31, 2020. For more information on Origin’s COVID-19 impacted sectors, please see the Investor Presentation furnished to the SEC on January 27, 2021, and on Origin's website at www.origin.bank under the Investor Relations, News & Events, Events & Presentations link.

The estimated impact and uncertain outcome of the COVID-19 pandemic led to an increase in classified assets as well as an increase in the allowance for loan credit losses. Classified loans as a percentage of LHFI, excluding PPP loans, and as a percentage of total risk-based capital (at the Origin Bancorp, Inc. level) were 2.08% and 12.88%, respectively, at December 31, 2020, reflecting an increase from 1.57% and 10.67%, respectively, at December 31, 2019.

Results of Operations for the Three Months Ended December 31, 2020

Net Interest Income and Net Interest Margin Net interest income for the quarter ended December 31, 2020, was $51.8 million, an increase of $1.2 million, or 2.4%, compared to the linked quarter. The increase was primarily due to a $1.5 million increase in income from mortgage warehouse lines of credit coupled with a $1.1 million reduction in total interest-bearing deposit expenses, offset by a $1.4 million decrease in interest earned on commercial and industrial loans and a $761,000 increase in subordinated debenture interest expense during the current quarter compared to the linked quarter.

Interest income on mortgage warehouse lines of credit increased by $1.5 million during the quarter ended December 31, 2020, compared to the linked quarter due to higher mortgage activity driven by the continued low interest rate environment, coupled with additional mortgage warehouse clients being onboarded and funding loans during 2020. Interest income earned on commercial and industrial loans, excluding PPP loans, decreased by $1.4 million during the quarter ended December 31, 2020, compared to the linked quarter due to a combination of the impact of lower interest rates and lower average balances, which contributed $883,000 and $478,000, respectively, to the decrease. Interest-bearing deposit expense was $4.6 million during the current quarter, compared to $5.7 million for the quarter ended September 30, 2020, primarily due to a reduction in deposit rates. The average rate on savings and interest-bearing transaction accounts was 0.29% for the current quarter, down from 0.39% for the linked quarter, accounting for $900,000 of the decrease in interest expense from the linked quarter. The average rate on time deposits decreased to 1.20% for the current quarter, down from 1.50% for the linked quarter, providing an additional decrease of $511,000 in interest expense. These two interest expense declines were offset by a $496,000 increase in interest expense due to an increase in the average balances of savings and interest-bearing transaction accounts when comparing the December 31, 2020, quarter to the linked quarter.

The fully tax-equivalent net interest margin ("NIM") was 3.07% for the current quarter, an 11 basis point decrease from the linked quarter and a 51 basis point decrease from the quarter ended December 31, 2019. Excluding PPP loans, the fully tax-equivalent NIM was 3.17%, also an 11 basis point decrease from the linked quarter. The yield earned on interestearning assets was 3.47%, a 17 basis point and a 109 basis point decrease compared to the linked quarter and the quarter ended December 31, 2019, respectively. Excluding PPP loans, the yield earned on interest-earning assets was 3.57%, an 18 basis point decrease compared to the linked quarter. The rate paid on total interest-bearing liabilities for the quarter ended December 31, 2020, was 0.64%, representing a decrease of 11 basis points and 82 basis points compared to the linked quarter and the quarter ended December 31, 2019, respectively. The Company has experienced margin compression since the quarter ended December 31, 2019, primarily caused by decreasing loan yields driven by declining short-term interest rates over the last several quarters.

Noninterest Income

Noninterest income for the quarter ended December 31, 2020, was $15.4 million, a decrease of $2.7 million, or 14.8%, from the linked quarter. The decrease from the linked quarter was primarily driven by a decrease of $2.9 million in mortgage banking revenue.

Mortgage banking revenue decreased primarily due to a $1.6 million decrease in volume-related gains and income and a $1.3 million decrease in hedge effectiveness. Mortgage servicing revenue hedge performance was lower during the quarter ended December 31, 2020, compared to the linked quarter, with only $68,000 net hedge effectiveness during the quarter ended December 31, 2020, compared to $1.4 million in net hedge effectiveness during the quarter ended September 30, 2020. Mortgage banking revenue increased $3.2 million, or 96.3%, from the quarter ended December 31, 2019.

Noninterest Expense

Noninterest expense for the quarter ended December 31, 2020, was $38.9 million, a slight increase of $150,000, compared to the linked quarter. The increase from the linked quarter was largely driven by an increase of $391,000 in professional services expense, which was offset by a decrease of $213,000 in other noninterest expense.

The increase in professional services expense was primarily driven by fees paid to a loan sale advisor who assisted in the sale of a performing loan during the quarter.

The decrease in other noninterest expense was largely due to a litigation accrual of $475,000 that was recorded during the quarter ended September 30, 2020, not recurring in the current quarter.

Financial Condition Loans

- Total LHFI increased $112.1 million compared to the linked quarter and $1.58 billion compared to December 31, 2019.

- PPP loans, net of deferred fees and costs, totaled $546.5 million at December 31, 2020, and decreased $5.8 million compared to the linked quarter.

- Average LHFI increased $164.0 million, compared to the linked quarter, and $1.29 billion compared to December 31, 2019.

Total LHFI at December 31, 2020, were $5.72 billion, reflecting an increase of 2.0% compared to the linked quarter and an increase of 38.2%, compared to December 31, 2019. The increase in LHFI was primarily driven by an increase in mortgage warehouse lines of credit and PPP loans when compared to December 31, 2019. Mortgage warehouse lines of credit increased by $809.3 million primarily due to increased mortgage activity driven by the continued low interest rate environment, coupled with additional mortgage warehouse clients being onboarded and funding loans during 2020.

Deposits

- Total deposits decreased $184.6 million compared to the linked quarter and increased $1.52 billion compared to December 31, 2019.

- Business depositors drove an increase of $691.0 million compared to the quarter ended December 31, 2019. • Average brokered deposits for the quarter ended December 31, 2020, increased by $344.2 million over the linked quarter and $489.6 million over the quarter ended December 31, 2019. Brokered deposits at December 31, 2020, decreased by $404.7 million compared to the linked quarter and increased $278.6 million compared to December 31, 2019.

- Average total deposits for the quarter ended December 31, 2020, increased by $508.7 million over the linked quarter and $1.68 billion over the quarter ended December 31, 2019.

Total deposits at December 31, 2020, were $5.75 billion, reflecting a decrease of 3.1% compared to the linked quarter and an increase of 36.0% compared to December 31, 2019. Brokered deposits declined by $404.7 million, offset by increases in interest-bearing demand and money market deposits of $145.7 million and $88.6 million, respectively, compared to the linked quarter. The Company has used noncore funding sources, including brokered deposits, to support the increase in mortgage warehouse lines of credit during 2020. In December 2020, due to changing rates on noncore funding options, the Company shifted some noncore funding from brokered deposits to FHLB advances, which has caused a decline in brokered deposit balances at December 31, 2020, when compared to September 30, 2020. Also, the Company was able to increase other deposits which contributed to the reduction in brokered deposits at December 31, 2020. Increases of $529.9 million, $512.9 million and $278.6 million in noninterest-bearing, money market and brokered deposits, respectively, drove the increase in total deposits compared to December 31, 2019, partially due to depositors moving into a statistically higher percentage of personal savings rates.

For the quarter ended December 31, 2020, average noninterest-bearing deposits as a percentage of total average deposits was 28.7%, compared to 30.4% for the quarter ended September 30, 2020, and 27.4% for the quarter ended December 31, 2019.

Borrowings

- Average FHLB advances and other borrowings for the quarter ended December 31, 2020, decreased by $193.7 million, compared to the quarter ended September 30, 2020, and decreased by $3.0 million over the quarter ended December 31, 2019.

- Average subordinated debentures increased $65.9 million for the quarter ended December 31, 2020, compared to the linked quarter and $134.8 million compared to the quarter ended December 31, 2019.

Average FHLB advances and other borrowings decreased 36.4% for the quarter ended December 31, 2020, compared to the quarter ended September 30, 2020, and decreased 0.9% compared to the quarter ended December 31, 2019. During the quarter ended September 30, 2020, the Company repaid $319.3 million of advances under the Federal Reserve's PPP Lending Facility which caused a decrease in average borrowings of $209.3 million during the quarter ended December 31, 2020.

In October 2020, the Company completed of an offering of $80.0 million in aggregate principal amount of 4.50% fixed-to floating rate subordinated notes due 2030. Additionally, in February 2020, Origin Bank completed an offering of $70.0 million in aggregate principal amount of 4.25% fixed-to-floating rate subordinated notes due 2030.

Stockholders' equity was $647.2 million at December 31, 2020, an increase of $19.5 million compared to $627.6 million at September 30, 2020, and an increase of $47.9 million compared to $599.3 million at December 31, 2019. The increase from the linked quarter was primarily due to net income for the quarter of $17.6 million. The increase from the December 31, 2019, quarter was primarily caused by retained earnings and other comprehensive income during the intervening period.

Conference Call

Origin will hold a conference call to discuss its fourth quarter and 2020 full year results on Thursday, January 28, 2021, at 8:00 a.m. Central Time (9:00 a.m. Eastern Time). To participate in the live conference call, please dial (844) 695-5516; International: (412) 902-6750 and request to be joined into the Origin Bancorp, Inc. (OBNK) call. A simultaneous audio-only webcast may be accessed via Origin's website at www.origin.bank under the Investor Relations, News & Events, Events & Presentations link or directly by visiting https://services.choruscall.com/links/obnk210128.html.

If you are unable to participate during the live webcast, the webcast will be archived on the Investor Relations section of Origin's website at www.origin.bank, under Investor Relations, News & Events, Events & Presentations.

About Origin Bancorp, Inc.

Origin is a financial holding company headquartered in Ruston, Louisiana. Origin's wholly owned bank subsidiary, Origin Bank, was founded in 1912. Deeply rooted in Origin's history is a culture committed to providing personalized, relationship banking to its clients and communities. Origin provides a broad range of financial services to businesses, municipalities, high net-worth individuals and retail clients. Origin currently operates 44 banking centers located from Dallas/ Fort Worth, Texas across North Louisiana to Central Mississippi, as well as in Houston, Texas. For more information, visit www.origin.bank.

Forward-Looking Statements

This press release contains certain forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements include information regarding Origin's future financial performance, business and growth strategy, projected plans and objectives, including the Company’s loan loss reserves and allowance for credit losses related to the COVID-19 pandemic and any expected purchases of its outstanding common stock, and related transactions and other projections based on macroeconomic and industry trends, including expectations regarding efforts to respond to the COVID-19 pandemic and continued low interest rates or interest rate cuts by the Federal Reserve and the resulting impact on Origin's results of operations, estimated forbearance amounts and expectations regarding the Company's liquidity, including in connection with advances obtained from the FHLB, which are all subject to change and may be inherently unreliable due to the multiple factors that impact broader economic and industry trends, and any such changes may be material. Such forwardlooking statements are based on various facts and derived utilizing important assumptions and current expectations, estimates and projections about Origin and its subsidiaries, any of which may change over time and some of which may be beyond Origin's control. Statements or statistics preceded by, followed by or that otherwise include the words "anticipates," "believes," "estimates," "expects," “foresees,” "intends," "plans," "projects," and similar expressions or future or conditional verbs such as "could," "may," “might,” "should," "will," and "would" or variations of such terms are generally forward-looking in nature and not historical facts, although not all forward-looking statements include the foregoing words. Further, certain factors that could affect Origin's future results and cause actual results to differ materially from those expressed in the forward-looking statements include, but are not limited to: the continuing duration and impacts of the COVID-19 global pandemic and continuing development and distribution of COVID-19 vaccines, as well as other efforts to contain the virus's transmission, including the effect of these factors and developments on Origin’s business, customers and economic conditions generally, as well as the impact of the actions taken by governmental authorities to address the impact of COVID-19 on the United States economy, including, without limitation, the Coronavirus Aid, Relief and Economic Security Act (the “CARES Act”) and any related future economic stimulus legislation; deterioration of Origin's asset quality; factors that can impact the performance of Origin’s loan portfolio, including real estate values and liquidity in Origin's primary market areas; the financial health of Origin's commercial borrowers and the success of construction projects that Origin finances; changes in the value of collateral securing Origin's loans; Origin’s ability to anticipate interest rate changes and manage interest rate risk; the effectiveness of Origin’s risk management framework and quantitative models; Origin’s inability to receive dividends from Origin Bank and to service debt, pay dividends to Origin’s common stockholders, repurchase Origin’s shares of common stock and satisfy obligations as they become due; business and economic conditions generally and in the financial services industry, nationally and within Origin's primary market areas; changes in Origin’s operation or expansion strategy or Origin's ability to prudently manage its growth and execute its strategy; changes in management personnel; Origin's ability to maintain important customer relationships, reputation or otherwise avoid liquidity risks; increasing costs as Origin grows deposits; operational risks associated with Origin’s business; volatility and direction of market interest rates; increased competition in the financial services industry, particularly from regional and national institutions; difficult market conditions and unfavorable economic trends in the United States generally, and particularly in the market areas in which Origin operates and in which its loans are concentrated; an increase in unemployment levels and slowdowns in economic growth; Origin's level of nonperforming assets and the costs associated with resolving any problem loans including litigation and other costs; the credit risk associated with the substantial amount of commercial real estate, construction and land development, and commercial loans in Origin's loan portfolio; changes in the laws, rules, regulations, interpretations or policies relating to financial institutions, and potential expenses associated with complying with such regulations, periodic changes to the extensive body of accounting rules and best practices; further government intervention in the U.S. financial system; compliance with governmental and regulatory requirements, including the Dodd-Frank Wall Street Reform and Consumer Protection Act and others relating to banking, consumer protection, securities and tax matters; Origin's ability to comply with applicable capital and liquidity requirements, including its ability to generate liquidity internally or raise capital on favorable terms, including continued access to the debt and equity capital markets; changes in the utility of Origin's non-GAAP liquidity measurements and its underlying assumptions or estimates; uncertainty regarding the future of the London Interbank Offered Rate and the impact of any replacement alternatives on Origin’s business; possible changes in trade, monetary and fiscal policies, laws and regulations and other activities of governments, agencies and similar organizations; natural disasters and adverse weather events, acts of terrorism, an outbreak of hostilities, regional or national protests and civil unrest (including any resulting branch closures or property damage), widespread illness or public health outbreaks or other international or domestic calamities, and other matters beyond Origin’s control; and system failures, cybersecurity threats or security breaches and the cost of defending against them. For a discussion of these and other risks that may cause actual results to differ from expectations, please refer to the sections titled "Cautionary Note Regarding Forward-Looking Statements" and "Risk Factors" in Origin's most recent Annual Report on Form 10-K filed with the Securities and Exchange Commission and any updates to those sections set forth in Origin's subsequent Quarterly Reports on Form 10-Q and Current Reports on Form 8-K. If one or more events related to these or other risks or uncertainties materialize, or if Origin's underlying assumptions prove to be incorrect, actual results may differ materially from what Origin anticipates. Accordingly, you should not place undue reliance on any forward-looking statements. Any forward-looking statement speaks only as of the date on which it is made, and Origin does not undertake any obligation to publicly update or review any forward-looking statement, whether as a result of new information, future developments or otherwise. New risks and uncertainties arise from time to time, and it is not possible for Origin to predict those events or how they may affect Origin. In addition, Origin cannot assess the impact of each factor on Origin's business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. Furthermore, many of these risks and uncertainties are currently amplified by and may continue to be amplified by or may, in the future, be amplified by, the outbreak of the COVID-19 pandemic and the impact of varying governmental responses, including the CARES Act, that affect Origin's customers and the economies where they operate. All forward-looking statements, expressed or implied, included in this communication are expressly qualified in their entirety by this cautionary statement. This cautionary statement should also be considered in connection with any subsequent written or oral forwardlooking statements that Origin or persons acting on Origin's behalf may issue. Annualized, pro forma, adjusted, projected and estimated numbers are used for illustrative purpose only, are not forecasts and may not reflect actual results. Contact: Chris Reigelman, Origin Bancorp, Inc. 318-497-3177 / chris@origin.bank